Guide to Supplementary Retirement Scheme (SRS): Part 2

Don't be blinded by the benefits of SRS! If you are a young adult, should you even contribute to SRS in the first place? Let me share my thoughts on this!

PERSONAL FINANCEINVESTMENTSSRS

If you are not familiar with the basics of SRS, read part 1 of my guide here.

There are many influencers out there advocating about possible SRS investment choices, but while I'm a fan of SRS, I think one should be mindful about contributing to SRS.

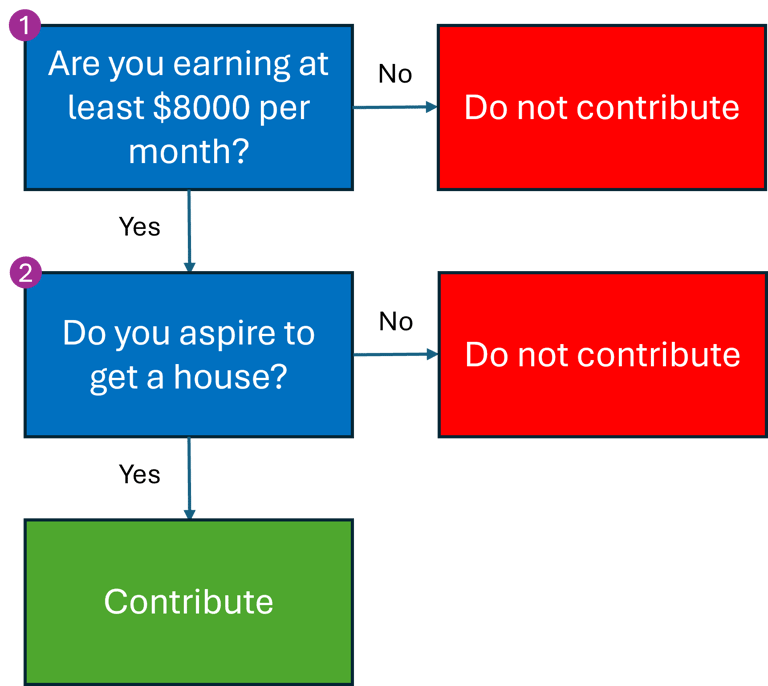

When does it make sense to contribute to SRS?

I've created the chart above to make it easier for everyone to understand the considerations for contributing to SRS.

High Income? Why don't you contribute to SRS?

The primary and immediate benefit of SRS is tax savings. If your income is not high enough in the first place, then your income taxes will not be high enough to justify contributing to SRS.

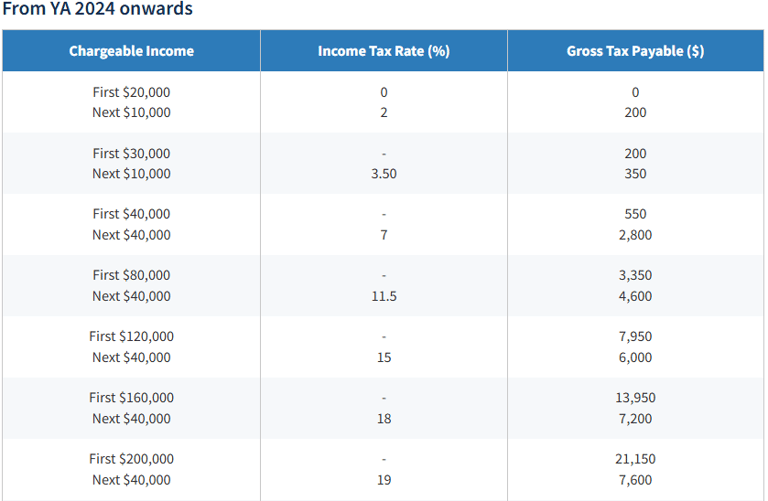

Let's run some numbers here. Assuming person A earns $8000 per month, and A also receives an annual bonus of 0.5 months, then A will be taking home $100000 annually.

Assuming that A also enjoys tax relief of $10000 from other sources, then A's chargeable income will be $90000, and his income tax bill will amount to $3350 + (11.5% * $10000) = $4500.

If A enjoys the $10000 in tax relief and had also contributed $15300 to SRS that year, his chargeable income will now be lower, at $74700, and he will be paying income tax of $550 + (7% * $34700) = $2979. He would have saved $4500 - $2979 = $1521. That is almost a ~10% 'gain' from his SRS contribution of $15300!

Now, moving on to person B, B earns an annual salary of just $80000 per year, inclusive of bonuses. B also enjoys a tax relief of $10000, and without any income tax contributions, he will be paying $550 + (7% * $30000) = $2650 in income taxes.

If B changes his mind and decides to contribute $15300 to his SRS account, and with his existing $10000 tax relief, his chargeable income is now $64700. B's income tax bill will now be lower at $550 + (7% * $24700) = $2279. B's tax savings thus amount to $2650 - $2279 = $371. That is a ~2.4% 'gain' derived from his $15300 contribution to SRS.

I'm not discouraging anyone from contributing to SRS, but it is clear that the tax savings from SRS are much more substantial when you earn a high income (at least $100000 annually).

Acquiring a property soon? Don't contribute to SRS!

It doesn't have to be a property, but if you foresee yourself having to commit to a large expense soon, then I would suggest not contributing to SRS.

Remember, the drawback of SRS is a lack of liquidity. If you need to use cash soon, then do not contribute to SRS.

I'm using housing as an example here, because housing is a necessity and is a big-ticket item. Most people aspire to own a home, and I think it makes a lot of sense to prioritise saving for a home before saving for retirement (via SRS).

For any young adult (below 35 years of age), if you are buying a private property that costs 1 million dollars, you will have to fork out $274600 in down payment and buyer stamp duty. Coupled with legal fees and other miscellaneous fees, you can expect to fork out approximately $290000 (in cash and CPF), which is not a small amount for any young adult. Hence, if you are looking to acquire a property soon, I recommend saving up for the property and not contributing to SRS.

Conclusion

I hope this article has made clear when does it make sense to contribute to SRS.

While SRS was designed to help Singaporeans retire by forming a secondary income stream complementing the CPF, one should consider your immediate needs (e.g. liquidity, and need of cash to fund a large purchase), and the tax efficiency (i.e. potential tax savings) before contributing to SRS.

Other Stories

Disclaimer: The content on this site is for informational purposes only and should NOT be taken as legal, business, tax or investment advice. The content does NOT constitute an offer or solicitation to purchase any investment.

This site does not take into account your personal financial situation or needs, and makes no representation and assumes no liability to the accuracy or completeness of the information provided here. This site shall not be liable for any losses that may arise as a result of the content published.

Want all of these in your inbox?

Subscribe to the newsletter and never miss a story.

We care about your data in our privacy policy.